Contents

- 1 Shadowfax IPO – GMP, Valuation, Financials, Review & Listing Outlook

- 1.1 📌 Shadowfax IPO Snapshot (Expected)

- 1.2 🏢 Company Overview

- 1.3 📊 Business Model & Revenue Mix

- 1.4 💰 Financial Summary (Indicative)

- 1.5 📊 Key Operating Metrics (KPIs)

- 1.6 💼 Funding & Investor Profile

- 1.7 📊 Valuation Outlook (Pre-IPO Model)

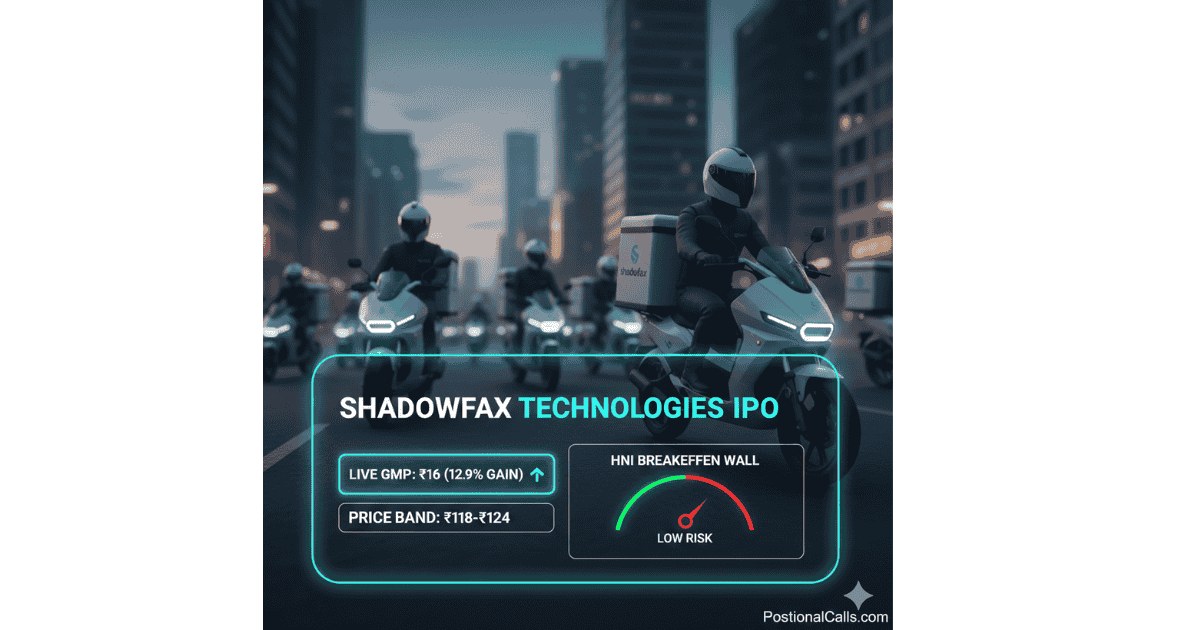

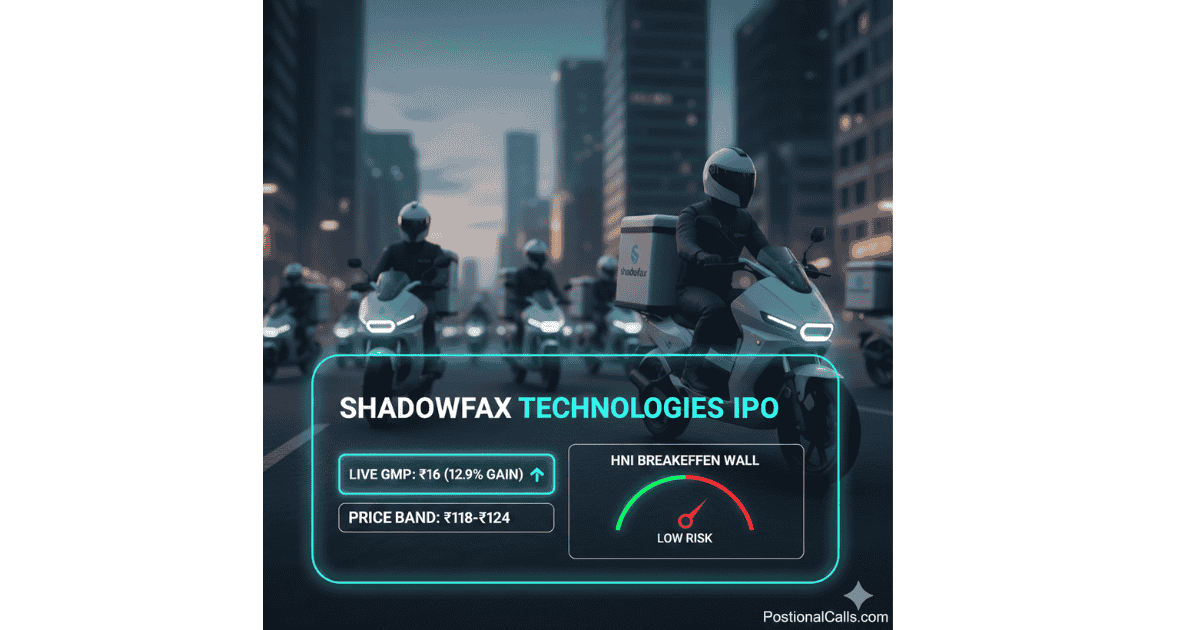

- 1.8 📈 Grey Market Premium (GMP) — Indicative

- 1.9 📊 Listing Scenario Model

- 1.10 📌 SWOT Analysis

- 1.11 ⚠️ Key Risks

- 1.12 👥 Who Should Apply?

- 1.13 📊 PositionalCalls IPO Scorecard

- 1.14 🏁 Final Verdict (Updated)

Shadowfax IPO – GMP, Valuation, Financials, Review & Listing Outlook

Shadowfax IPO is one of the most anticipated logistics-tech listings in India. This page acts as a complete IPO intelligence hub covering expected issue details, fundamentals, valuation models, financial trends, risks, peers, sentiment signals, and listing outlook.

• IPO Type: Mainboard IPO (Expected)

• Sector: Logistics & Hyperlocal Delivery

• Investor Sentiment: Neutral → Cautiously Positive

• Market Reaction: Mixed (growth strong, margins thin)

• Risk Level: Medium–High (Tech-Logistics Model)

• Listing Outlook: Highly dependent on valuation and QIB demand

🚨 Latest Update — PositionalCalls Intelligence Desk

Market Movement:

• Shadowfax continues to remain among the most tracked upcoming IPOs in India’s startup ecosystem amid rising interest in logistics and quick-commerce companies.

Investor Sentiment Shift:

• Sentiment has gradually shifted from Neutral → Cautiously Positive due to improving profitability trends and strong growth in hyperlocal deliveries.

Market Reaction:

• Institutional investors are expected to focus on valuation discipline, while retail investors may react strongly to brand recognition and growth narrative.

Sector Signal:

• Logistics and quick-commerce IPOs are emerging as a key market theme in India, supported by digital consumption and last-mile delivery demand.

Why this matters:

• Recent tech IPOs show that valuation comfort and QIB participation are the biggest drivers of listing performance.

Historical patterns from new-age tech IPOs indicate that Shadowfax’s listing outcome will depend more on valuation and institutional demand than hype. If priced aggressively, listing volatility is likely; if priced reasonably, strong subscription and premium listing probability increase.

Is Shadowfax the next big logistics IPO story or a high-risk startup bet? Can rapid growth offset thin margins? Here is a data-driven IPO analysis and apply-or-avoid framework.

📌 Shadowfax IPO Snapshot (Expected)

| Parameter | Details |

|---|---|

| Company Name | Shadowfax Technologies Limited |

| Sector | Logistics & Hyperlocal Delivery |

| IPO Type | Mainboard IPO (Expected) |

| Issue Size | ₹2,000 – ₹3,500 Crore (Market Estimates) |

| Fresh Issue | ₹1,000 – ₹1,800 Crore (Expected) |

| OFS | ₹1,000 – ₹1,700 Crore (Expected) |

| IPO Timeline | 2026–2027 (Expected) |

| Listing Exchange | NSE & BSE |

| Registrar | Likely KFin Technologies / Link Intime |

| Expected Valuation | ₹8,000 – ₹12,000 Crore |

🏢 Company Overview

Shadowfax is a technology-driven last-mile logistics platform serving e-commerce, quick commerce, and enterprise clients across India. The company operates an asset-light delivery model supported by a large gig workforce and AI-driven routing systems.

| Metric | Details |

|---|---|

| Founded | 2015 |

| Headquarters | Bengaluru, India |

| Network Coverage | 4,000+ cities & towns |

| Service Reach | 14,000+ PIN codes |

| Delivery Partners | 1 Million+ gig workforce (approx) |

| Key Clients | Flipkart, Meesho, Myntra, D2C brands |

| Business Focus | Last-mile & quick commerce logistics |

📊 Business Model & Revenue Mix

| Segment | Description | Approx Share |

|---|---|---|

| Express Logistics | E-commerce deliveries | ~65%–70% |

| Quick Commerce | Hyperlocal instant delivery | ~20%–25% |

| Enterprise & Others | B2B, pharma, D2C logistics | ~10%–15% |

💰 Financial Summary (Indicative)

| Year | Revenue (₹ Cr) | EBITDA Margin | PAT (₹ Cr) |

|---|---|---|---|

| FY2023 | 1,415 | -7.1% | -142.6 |

| FY2024 | 1,885 | 1.0% | -11.9 |

| FY2025 | 2,485 | 1.9% | +6.4 |

| H1 FY2026 | 1,820 | 2.8% | +21.0 |

Insight: Shadowfax is transitioning from losses to profitability, but margins remain thin compared to traditional logistics companies.

📊 Key Operating Metrics (KPIs)

| Metric | Value |

|---|---|

| Annual Shipments | 500+ million parcels (estimated) |

| Revenue per Shipment | ₹40 – ₹55 |

| Customer Retention | High (Top clients recurring) |

| Cost per Delivery | ₹35 – ₹48 |

| Contribution Margin | Low but improving |

💼 Funding & Investor Profile

| Investor | Type |

|---|---|

| Flipkart | Strategic Investor |

| Eight Roads Ventures | VC |

| Nokia Growth Partners | VC |

| Qualcomm Ventures | VC |

📊 Valuation Outlook (Pre-IPO Model)

| Company | Business | EBITDA Margin | Valuation Trend |

|---|---|---|---|

| Shadowfax (Expected) | Hyperlocal Logistics | ~1%–3% | Premium |

| Delhivery | Integrated Logistics | ~4%–6% | High |

| Blue Dart | Premium Logistics | ~15%–18% | Moderate |

| Ecom Express | E-commerce Logistics | ~3%–5% | Mid |

📈 Grey Market Premium (GMP) — Indicative

Expected GMP Range (Pre-IPO): ₹8 – ₹15 (Indicative)

Grey Market Sentiment: Neutral to Mild Positive

Interpretation: Listing gains depend heavily on final IPO pricing and institutional demand.

📊 Listing Scenario Model

| Scenario | IPO Pricing | Expected Listing Outcome |

|---|---|---|

| Bull Case | Reasonable valuation | +20% to +45% |

| Base Case | Premium valuation | +5% to +15% |

| Bear Case | Overvalued IPO | -5% to +5% |

📌 SWOT Analysis

| Factor | Details |

|---|---|

| Strength | Fast growth, asset-light model, strong tech platform |

| Weakness | Thin margins, high dependency on e-commerce clients |

| Opportunity | Quick commerce boom, D2C logistics demand |

| Threat | Intense competition, rising fuel & labor costs |

⚠️ Key Risks

| Risk | Impact |

|---|---|

| Thin Profit Margins | Limits long-term valuation |

| High Client Concentration | Revenue volatility |

| Intense Competition | Pressure on pricing |

| Fuel & Labour Costs | Margin erosion |

| Valuation Risk | Flat listing possibility |

👥 Who Should Apply?

| Investor Type | Recommendation | Reason |

|---|---|---|

| Retail Investors | Speculative Apply | Listing gains only |

| sNII (Small HNI) | Selective | Depends on GMP & pricing |

| bNII (Big HNI) | Cautious | Avoid high leverage |

| Long-Term Investors | Wait & Watch | Profitability still evolving |

📊 PositionalCalls IPO Scorecard

| Business Growth | 8.2 / 10 |

| Financial Strength | 5.6 / 10 |

| Valuation Comfort | 4.3 / 10 |

| Risk Level | High ⚠️ |

| Overall Score | 6.2 / 10 |

🏁 Final Verdict (Updated)

Shadowfax IPO represents a high-growth but high-risk logistics opportunity. While revenue growth is strong and the company is moving toward profitability, thin margins and aggressive valuation could limit long-term returns. Investors should treat this IPO primarily as a listing-gain opportunity unless pricing is attractive.

Shadowfax IPO reflects the new-age tech-logistics cycle where growth potential is strong but valuation discipline will determine listing success.

Disclaimer: Shadowfax IPO details are based on market estimates and publicly available information. IPO investments involve market risks. This content is for educational purposes only and does not constitute financial advice.

READ MORE: Digilogic Systems IPO GMP Today — Live Grey Market Premium & Expert View

Shubham tracks Indian equity markets with a focus on banking stocks, insurance companies, and long-term value investing. PositionalCalls was built to give independent investors the same quality of research that institutional desks produce — in plain language, with no brokerage bias and no paid promotions. All analysis is sourced from RBI, SEBI, NSE/BSE filings, and company annual reports.