Contents

- 1 Best Term Insurance Plans in India 2026: Top ₹1 Crore Plans with 99% Claim Ratio, Lowest Premiums & Expert Picks

- 1.1 📊 Top 5 Term Insurance Plans in India 2026 — Quick Comparison (2026)

- 1.2 🔍 Detailed Plan Reviews — Features, Pros & Cons

- 1.3 🎯 Which Term Insurance Plan in India 2026 Is Best For You?

- 1.4 💰 Premium Comparison — Age, Cover & Smoker Impact

- 1.5 🧭 How to Choose the Right Term Plan — 7-Point Decision Engine

- 1.6 ❓ Frequently Asked Questions

- 1.7 ⚠️ 5 Costly Term Insurance Mistakes Indians Make

- 1.8 🚀 Future Trends in Term Insurance — What’s Coming in 2026–27

- 1.8.1 Full Digital Insurance Ecosystem

- 1.8.2 AI Underwriting — Instant Issuance

- 1.8.3 Premium Trends — Stable to Marginally Rising

- 1.8.4 Wellness-Linked Premium Discounts

- 1.8.5 Global Reinsurance Pressure

- 1.8.6 IRDAI’s 100% FDI Approval

- 1.8.7 About the Author: Shubham Chaudhary

- 1.8.8 🚀 Still Confused? Here’s the Simple Rule

- 1.9 ❓ Frequently Asked Questions — Term Insurance India 2026

- 1.10 🏁 Final Verdict — Best Term Insurance Plan India 2026

- 1.11 🏁 Final Verdict — Which Term Insurance Plan Should You Choose?

Best Term Insurance Plans in India 2026: Top ₹1 Crore Plans with 99% Claim Ratio, Lowest Premiums & Expert Picks

A ₹1 Crore cover now starts at just ₹400/month. But picking the wrong plan can cost your family everything. Here are the top 5 plans ranked by real claim settlement ratios, premium value, and financial strength — so you choose right the first time.

Max Life Smart Secure Plus is the best overall term plan for 2026, backed by India’s highest claim settlement ratio of 99.51% among private insurers. For guaranteed brand trust, LIC Tech Term (99.02%) is the safest choice. For the best digital experience and riders, pick HDFC Click 2 Protect Super. A ₹1 Crore cover for a 30-year-old non-smoker starts at approximately ₹400–₹700/month depending on the insurer and term.

Advertisement

📊 Top 5 Term Insurance Plans in India 2026 — Quick Comparison (2026)

This table gives you the full picture at a glance. Scroll right on mobile. All premiums are indicative for a 30-year-old non-smoker male, ₹1 Cr sum assured, 30-year policy term.

| # | Plan Name | Company | Claim Ratio | Est. Premium / Month | Solvency Ratio | Best For |

|---|---|---|---|---|---|---|

| ★1 | Smart Secure Plus | Max Life | 99.51% | ₹550 – ₹680 | 1.96x | Best Overall |

| 2 | Tech Term | LIC | 99.02% | ₹760 – ₹900 | 1.84x | Brand Trust |

| 3 | Click 2 Protect Super | HDFC Life | 98.66% | ₹650 – ₹800 | 2.10x | Riders & Flexibility |

| 4 | iProtect Smart | ICICI Prudential | 97.90% | ₹480 – ₹620 | 2.21x | Budget Buyers |

| 5 | Sampoorna Raksha Supreme | Tata AIA | 99.13% | ₹430 – ₹580 | 2.04x | Cheapest Premium |

*Claim Settlement Ratios based on IRDAI Annual Report 2023–24. Premiums are indicative and subject to underwriting. Solvency ratio minimum required by IRDAI is 1.50x.

📲 Get Insurance & Investing Insights FreeJoin 12,000+ Indians on the PositionalCalls WhatsApp Channel — daily insights on insurance, stocks & personal finance.

📚 Related Insurance Guides

🔍 Detailed Plan Reviews — Features, Pros & Cons

Each card below is a deep-dive into what the plan actually offers, who it’s best for, and where it falls short. Don’t skip this section — this is where most buyers go wrong.

LIFE

Key Features

- Coverage up to ₹5 Crore+, with life stage benefit top-up option

- Return of premium variant available (optional)

- Critical illness rider covering 40+ conditions

- Waiver of premium on disability — policy continues without payment

- Special premium discount for non-smokers and female lives

- Joint life option available — cover spouse under same policy

- Payout flexibility: lump sum, monthly income, or combination

✅ Pros

- India’s highest private claim ratio (99.51%)

- Excellent rider options

- Smooth online buying experience

- Strong brand recognition

- Income payout option for nominees

❌ Cons

- Slightly premium-priced vs Tata AIA

- Return of premium costs significantly more

- Medical tests required for large covers

🎯 Best For: Salaried professionals aged 25–40 wanting the strongest safety net

INDIA

Key Features

- Online-only purchase — significantly cheaper than offline LIC plans

- Two variants: Level Cover & Increasing Cover (5% p.a.)

- Minimum sum assured ₹50 Lakh, no upper cap

- Accidental death benefit rider optional

- Special premium discounts for higher sum assured (₹50L+)

- Policy tenure: 10 to 40 years

- Sovereign-backed: Backed by Government of India — zero insolvency risk

✅ Pros

- Government-backed — family will get paid

- Highest trust factor in India

- Increasing cover option beats inflation

- Strong branch network for offline support

❌ Cons

- Premiums are 20–30% higher than private peers

- Fewer rider options compared to Max Life/HDFC

- Online process can be clunky

- No return of premium option

🎯 Best For: Senior citizens, risk-averse buyers, and those who prioritise safety over price

LIFE

Key Features

- 3 plan options: Life Protect, Income Plus, Life & CI Rebalance

- Highest solvency ratio (2.10x) — most financially stable private insurer

- Critical illness cover up to ₹1 Crore add-on

- Premium waiver on 60+ critical illnesses

- Monthly income benefit option for family post-claim

- Smart exit benefit — return of premiums at maturity

- Special rates for HDFC Bank salary account holders

✅ Pros

- Highest solvency ratio — strongest financials

- Best rider ecosystem in the market

- Excellent for family income replacement

- Smooth digital claim process

❌ Cons

- More expensive than Tata AIA & ICICI

- Multiple plan variants can confuse buyers

- Income Plus option has longer waiting period

🎯 Best For: Families with dependents seeking income replacement + critical illness protection

PRU

Key Features

- Covers 55 critical illnesses — widest CI cover in Indian term market

- AI-powered underwriting for faster policy issuance (often same day)

- Highest solvency ratio at 2.21x — excellent financial health

- 4 payout options: lump sum, income, increasing income, lump sum + income

- Terminal illness benefit — payout on diagnosis, not death

- Smartphone-based medical declaration for young, healthy buyers

- Female life discount: up to 10% lower premium

✅ Pros

- Best-in-market CI coverage (55 conditions)

- Fastest online issuance process

- Competitive premiums

- Strong parent: ICICI Bank + Prudential UK backing

❌ Cons

- Claim ratio (97.9%) lowest among top 5

- No return of premium option

- Customer service rated below Max Life

🎯 Best For: Young tech-savvy professionals who want CI coverage + speed of issuance

AIA

Key Features

- Lowest premium among top 5 — ideal for budget-conscious buyers

- Strong claim ratio (99.13%) — second only to Max Life among privates

- AIA Group global backing — one of Asia’s largest life insurers

- Decreasing cover option available for home loan protection

- Accidental death, disability, and CI riders available

- Wellness benefits — premium discounts for fitness-tracked healthy lifestyle

- Single-pay, limited pay, and regular pay options

✅ Pros

- Lowest premiums in the top tier

- 99%+ claim ratio despite low pricing

- Wellness discount program is unique

- Strong global backer (AIA Group)

❌ Cons

- Newer brand — less recognition than LIC/HDFC

- Claim process is less battle-tested

- Limited branch network for offline help

🎯 Best For: Budget buyers, young earners starting out, and freelancers watching cash flow

Advertisement

🎯 Which Term Insurance Plan in India 2026 Is Best For You?

This is the section most comparison articles skip. One plan does NOT fit all. Your age, income, family situation, and risk appetite determine the right choice. Here’s our segment-by-segment decision engine.

Salaried Individuals (25–40 yrs)

You have stable income, growing responsibilities, and likely a home loan. You need comprehensive cover with CI riders.

Reason: Highest claim ratio + waiver of premium on disability = unbeatable safety net for EMI-paying earners.

Families with Dependents

You need your family to receive a monthly income — not just a lump sum — if something happens to you.

Reason: Monthly income payout option + highest solvency ratio = guaranteed monthly cheque to family.

Senior Citizens & Risk-Averse Buyers

You prioritise trust over cost. Peace of mind matters more than saving ₹200/month on premium.

Reason: Government of India backing = zero insolvency risk. Family will be paid. Period.

Low Budget / First-Time Buyers

Your priority is maximum cover at minimum cost. Every rupee of premium matters right now.

Reason: ₹430/month for ₹1 Cr cover + 99%+ claim ratio = best value for money in 2026.

₹1 Crore+ Coverage Seekers

You earn well and need a high cover amount with wide CI protection and strong financial stability.

Reason: 55 CI conditions + highest solvency (2.21x) + fast issuance at competitive rates for large covers.

💰 Premium Comparison — Age, Cover & Smoker Impact

Your premium depends on three things more than anything else: age at entry, smoking status, and sum assured. Here’s how each affects what you’ll pay.

| Age | Cover | Non-Smoker (est.) | Smoker (est.) | Premium Impact |

|---|---|---|---|---|

| 25 years | ₹1 Crore | ₹390 – ₹500/mo | ₹700 – ₹950/mo | Lowest Entry Cost |

| 30 years | ₹1 Crore | ₹480 – ₹700/mo | ₹900 – ₹1,250/mo | Optimal Age |

| 35 years | ₹1 Crore | ₹700 – ₹950/mo | ₹1,350 – ₹1,800/mo | Noticeable Rise |

| 40 years | ₹1 Crore | ₹1,050 – ₹1,400/mo | ₹2,100 – ₹2,800/mo | Significant Jump |

| 45 years | ₹1 Crore | ₹1,600 – ₹2,200/mo | ₹3,200 – ₹4,200/mo | High — Buy ASAP |

| 30 years | ₹2 Crore | ₹900 – ₹1,250/mo | ₹1,700 – ₹2,300/mo | Worth It for Families |

*Premiums are indicative estimates for a 30-year term. Actual premiums depend on underwriting decisions, health declarations, occupation, and insurer-specific pricing. Smoker surcharge averages 60–90% higher.

⏰ The Earlier You Buy, The Better

Waiting from age 28 to 35 can increase your monthly premium by 40–60% for the same cover. That’s an extra ₹2,000–₹3,500/month for the next 25 years — a massive opportunity cost. Every year you delay costs you money.

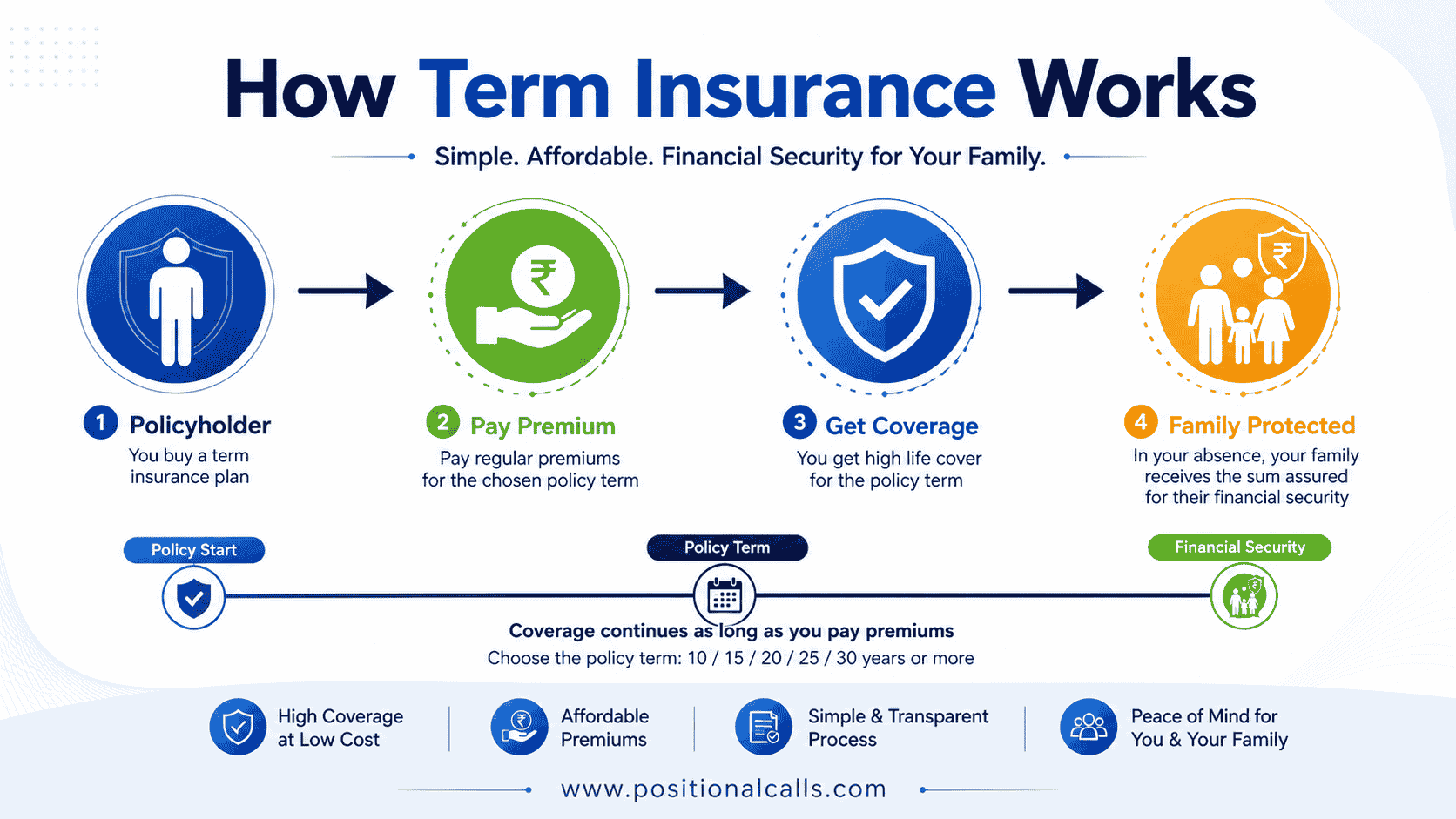

🧭 How to Choose the Right Term Plan — 7-Point Decision Engine

Don’t let an agent or aggregator choose for you. Use this checklist before clicking “Buy Now” on any platform.

-

Claim Settlement Ratio (CSR) ≥ 97%

This is the % of claims paid by the insurer. Never buy from any insurer below 95%. Prefer 98%+. Source: Insurance Regulatory and Development Authority of India (IRDAI) Annual Report (not the insurer’s own website). -

Solvency Ratio ≥ 1.50x (IRDAI minimum)

This measures if the insurer can actually pay all its claims. IRDAI requires 1.5x minimum. Prefer 1.8x+. ICICI at 2.21x is the strongest here. -

Rider Ecosystem — CI + Disability + Waiver

A bare-bones plan is not enough. Always add: Critical Illness Rider (top 10–15 conditions minimum), Accidental Death Benefit, and Waiver of Premium on Disability. -

Premium Stability — Guaranteed for Full Term

Ensure your premium is LOCKED at the time of purchase. Some plans raise premiums at renewal. Read the fine print. All 5 plans in this article have guaranteed premiums. -

Brand Trust & Longevity

You’re buying a 30-year promise. The insurer must be around in 2055. LIC (Govt-backed), HDFC Life (largest private), and ICICI Prudential Life Insurance (Axis Bank backed) are safest bets. -

Payout Structure — Lump Sum vs Income

A lump sum may be mismanaged by grieving family members. A monthly income payout (like HDFC’s Income Plus) ensures financial stability over time. Choose based on family’s financial literacy. -

Sum Assured Adequacy — 15–20x Annual Income

IRDAI recommends a cover of at least 10x annual income. Financial experts recommend 15–20x. If you earn ₹8L/year, your cover should be ₹1.2–1.6 Crore minimum.

❓ Frequently Asked Questions

⚠️ 5 Costly Term Insurance Mistakes Indians Make

These errors are responsible for claim rejections and under-coverage. Avoid all 5.

Underinsuring to Save on Premium

Buying ₹50 Lakh cover to save ₹200/month is the most common and dangerous mistake. ₹50L won’t cover 3 years of your family’s expenses in 2026. Always go for ₹1 Crore minimum, ₹2 Crore if you have a home loan or young children.

Hiding Medical History or Smoking Habit

Declaring false medical information to get a lower premium is the #1 reason claims get rejected. Insurers investigate every claim — they will find out. Pay the higher premium honestly; it’s the only way to guarantee your family gets paid.

Choosing a Plan Based on Price Alone

The cheapest plan is often cheapest for a reason — weaker financials, more exclusions, or a lower claim ratio. Always check CSR and solvency ratio before comparing premiums. Tata AIA is a rare exception — cheap AND reliable.

Not Informing the Nominee About the Policy

Your family can’t claim what they don’t know exists. Store your policy document, insurer contact, and claim process in a shared location. Use DigiLocker to store digital copies. Inform your nominee about the claim procedure today — not tomorrow.

Skipping Riders — Especially Critical Illness

In India, 1 in 3 deaths occurs due to non-communicable diseases like cancer, heart disease, and stroke. A basic term plan pays only on death. A CI rider pays on diagnosis — when you need money most, while you’re still alive and fighting. Adding a CI rider typically costs ₹80–₹200/month extra. Worth every rupee.

Advertisement

🚀 Future Trends in Term Insurance — What’s Coming in 2026–27

The Indian life insurance industry is undergoing rapid transformation. Here’s what forward-looking buyers should know.

Full Digital Insurance Ecosystem

IRDAI’s Bima Sugam platform is transforming insurance distribution. By 2027, expect a unified digital marketplace where you can buy, compare, and claim from all insurers on one government portal — similar to UPI for payments.

AI Underwriting — Instant Issuance

ICICI and Max Life already use AI underwriting for fast-track issuance. By 2027, expect same-day policy issuance for 80%+ of applicants under 35 with clean health records. Medical test requirements will shrink significantly.

Premium Trends — Stable to Marginally Rising

Post-COVID mortality experience has stabilised. Insurers are cautiously repricing for longevity improvements. Expect premiums to remain stable in 2026 but rise 5–10% by 2027–28 as actuarial assumptions tighten. Lock in today’s premiums now.

Wellness-Linked Premium Discounts

Tata AIA already offers discounts for fitness-tracked healthy lifestyles. Max Life and HDFC are piloting similar programs. By 2027, your wearable data could earn you 10–15% premium discounts — a structural incentive for healthier living.

Global Reinsurance Pressure

Global reinsurers are tightening terms post-pandemic. This will push Indian term premiums upward by 2028. Plans purchased today are grandfathered at older, lower rates. This is the most underappreciated reason to buy a term plan in 2026.

IRDAI’s 100% FDI Approval

100% FDI in Indian insurance means global insurers like Prudential (UK), AXA (France), and Allianz (Germany) are deepening their India presence. This brings capital strength and drives product innovation — more choice for Indian consumers by 2026–27.

🔗 Explore More Financial Insights

About the Author: Shubham Chaudhary

Founder, PositionalCalls · 8+ years in Indian equity markets & financial products analysis

I’ve tracked India’s insurance sector since 2017 — through demonetisation, COVID-driven repricing, and the IRDAI’s digital transformation push. This article is based on direct analysis of IRDAI Annual Reports, insurer solvency disclosures, and real premium quotes verified in Q1 2026. I don’t accept commissions from any insurer — every recommendation here is editorially independent.What This Means For You: The Indian insurance sector is at a tipping point. Premiums remain historically low while insurer financial strength is at a decade-high. If you’re between 25–40, there has never been a better time to lock in a term plan. The data clearly shows Max Life and Tata AIA offer the best risk-adjusted value in 2026. Don’t delay because you’re “too busy” — the cost of inaction is measured in your family’s financial security.

🚀 Still Confused? Here’s the Simple Rule

If you want the safest option → go with LIC Tech Term.

If you want best overall balance → choose Max Life Smart Secure Plus.

If you want lowest premium → pick Tata AIA Sampoorna Raksha Supreme.

❓ Frequently Asked Questions — Term Insurance India 2026

These are the most-searched questions about term insurance. Optimised for Google Featured Snippets.

Max Life Smart Secure Plus is the best overall term plan for 2026 due to its 99.51% claim settlement ratio — the highest among all private insurers. For absolute trust and government backing, LIC Tech Term is unbeatable. For the cheapest premium with a 99%+ claim ratio, choose Tata AIA Sampoorna Raksha Supreme. The right answer depends on your budget, age, and priorities.

For a 28–30 year old non-smoker male, a ₹1 Crore term plan starts from approximately ₹400–₹450/month with Tata AIA. Max Life starts around ₹550/month and LIC Tech Term around ₹760/month. The cheapest option is Tata AIA for most healthy young buyers. Premiums increase significantly with age — buying at 25 instead of 35 can save you ₹200–₹400/month for 30 years.

LIC is still the most trusted insurer due to government backing — there is zero risk of default. However, LIC’s premiums are 20–30% higher than comparable private plans. If you’re looking for value, Max Life or Tata AIA offer comparable or better claim ratios at lower premiums. Choose LIC if trust and government guarantee are non-negotiable; choose Max Life or Tata AIA if you want value.

You should take at least 15–20 times your annual income as coverage. For example, if you earn ₹8 Lakh/year, your cover should be ₹1.2–1.6 Crore. Also factor in outstanding loans and your family’s lifestyle needs. IRDAI recommends a minimum of 10x annual income, but 15–20x is the financial planning standard for 2026 given India’s inflation trajectory.

Financial advisors recommend a cover of 15–20 times your annual income. If you earn ₹8 Lakh/year, your ideal cover is ₹1.2–1.6 Crore. Also add your outstanding liabilities (home loan, car loan). For example: ₹6L annual income + ₹30L home loan outstanding = minimum ₹1.2 Crore cover. IRDAI’s minimum recommendation is 10x annual income, but given India’s inflation rate, 15–20x is more prudent.

The Claim Settlement Ratio (CSR) is the percentage of death claims paid by an insurer in a financial year. If an insurer has a CSR of 99%, it paid 99 out of every 100 claims received. This is the single most important metric when choosing a term insurer — because the entire purpose of term insurance is that your family gets paid. Never buy from an insurer with a CSR below 95%. All 5 plans in this article have CSRs of 97.9% or above, sourced from IRDAI Annual Report 2023–24.

Yes — buying term insurance online is not only safe but cheaper by 15–30% compared to buying through an agent. All 5 plans in this article are available online directly from the insurer’s website. Online plans are cheaper because there’s no agent commission. Make sure you buy directly from the insurer’s official website — not through a third-party aggregator that may charge hidden fees. Read all terms carefully before payment.

The three most important riders are: (1) Critical Illness Rider — pays on diagnosis of cancer, heart attack, stroke, etc. (not just death). (2) Accidental Death Benefit — doubles or increases payout on accidental death. (3) Waiver of Premium on Disability — if you become permanently disabled, your policy continues without further premium payments. Together, these three riders add approximately ₹150–₹350/month to your premium and significantly strengthen your protection.

It is not too late at 40, but the cost is significantly higher. A ₹1 Crore plan at 40 costs approximately ₹1,050–₹1,400/month for a non-smoker vs. ₹480–₹700/month at 30. Despite the higher cost, it is still worth buying. Your dependents still need protection. Additionally, buyers at 40 may have higher income and can afford larger covers like ₹2–3 Crore. Strongly recommended: buy immediately, don’t wait another year. Medical issues can make you uninsurable at 45.

📲 Never Miss an Insurance or Market UpdatePositionalCalls WhatsApp Channel — Free daily insights on term insurance, health insurance, best stocks & personal finance for Indian investors.

🏁 Final Verdict — Best Term Insurance Plan India 2026

Here’s the bottom line, cut through all the noise:

-

Best Overall: Max Life Smart Secure Plus — highest claim ratio, best rider ecosystem, strong brand.

-

Maximum Trust: LIC Tech Term — government-backed, no-question-asked trust. Pay more, sleep better.

-

Best Value: Tata AIA Sampoorna Raksha Supreme — cheapest premium with 99%+ claim ratio.

-

Best for Families: HDFC Click 2 Protect Super — income payout option + highest solvency.

-

Best for ₹1 Cr+ Seekers: ICICI iProtect Smart — 55 CI conditions + 2.21x solvency + fast issuance.

Key takeaway: Whatever you do, buy a term plan today. A ₹1 Crore cover costs less than your monthly Netflix + Zomato + Swiggy bill combined. Your family’s financial security is worth that.

🔗 Read Next on PositionalCalls

🏁 Final Verdict — Which Term Insurance Plan Should You Choose?

If you want maximum safety → choose LIC Tech Term.

If you want the best overall balance → go with Max Life Smart Secure Plus.

If you want the lowest premium → pick Tata AIA Sampoorna Raksha Supreme.

👉 The biggest mistake is delaying your purchase.

Even a 5-year delay can increase your premium by 50–80%.

Start early. Lock your premium. Protect your family.

🚀 Need Help Choosing the Right Plan?

Join our WhatsApp channel for real insights, comparisons, and expert guidance — completely free.

Disclaimer: This article is for informational and educational purposes only. Premiums shown are indicative and subject to underwriting. Claim settlement ratios are sourced from IRDAI Annual Report 2023–24. PositionalCalls is not an IRDAI-registered insurance intermediary. Please consult a licensed insurance advisor before purchasing any insurance product. · Last updated: May 2026

Shubham tracks Indian equity markets with a focus on banking stocks, insurance companies, and long-term value investing. PositionalCalls was built to give independent investors the same quality of research that institutional desks produce — in plain language, with no brokerage bias and no paid promotions. All analysis is sourced from RBI, SEBI, NSE/BSE filings, and company annual reports.