Contents

- 1 Best Family Health Insurance Plans India 2026

- 1.1 Why Family Health Insurance Is Critical in 2026

- 1.2 Best Family Health Insurance Plans India 2026: Quick Comparison Table

- 1.3 Which Plan Should YOU Choose? (Decision Engine)

- 1.4 Top 7 Best Family Health Insurance Plans in India 2026 — Full Reviews

- 1.5 Which Health Insurance Actually Pays Claims Smoothly in 2026?

- 1.6 How to Choose the Best Family Health Insurance Plan in 2026

- 1.7 How We Selected These Plans (Our Methodology)

- 1.8 Best Family Health Insurance Plans by Use Case

- 1.9 Family Floater vs Individual Health Insurance Policies

- 1.10 Tax Benefits Under Section 80D: Complete 2026 Guide

- 1.11 Claim Settlement & Cashless Network Analysis 2026

- 1.12 Common Exclusions & Costly Buyer Mistakes

- 1.13 How We Ranked These Plans (Methodology)

- 1.14 FAQ — Best Family Health Insurance Plans India 2026: 18 Top Questions

- 1.15 Glossary: Key Health Insurance Terms Explained

- 1.16 Final Expert Verdict: Best Family Health Insurance Plans India 2026

Best Family Health Insurance Plans India 2026

India’s most authoritative guide to family floater plans — comparing premiums, cashless hospital networks, maternity benefits, PED waiting periods, restoration clauses and Section 80D tax savings across India’s top 7 insurers. 13% medical inflation makes the right choice more critical than ever.

🏆 Top Picks (2026) — Quick Decision

- Best Overall: Niva Bupa ReAssure 2.0 — Unlimited restoration + 91.2% CSR

- Best Premium Coverage: HDFC ERGO Optima Secure — 92.7% CSR + 4× SI boost

- Best for Maternity: Care Supreme Floater — 24-month PED + 19,000+ cashless hospitals

- Best Budget: Star Family Health Optima — Lowest premium for Tier-2/3 cities

Why Family Health Insurance Is Critical in 2026

If you want the best family health insurance in India in 2026, choose based on your profile — not just rankings. For most families, Niva Bupa ReAssure 2.0 offers the best balance of coverage and value, while HDFC ERGO Optima Secure is ideal for maximum coverage and Care Supreme Floater works best for maternity-focused planning.

Best family health insurance plans India 2026 are essential for families seeking affordable premiums, strong claim settlement ratios, maternity benefits, and maximum financial protection. India’s healthcare costs are no longer a background concern — they are a foreground financial emergency. Medical inflation in India is projected at 13% in 2026, more than three times the general CPI inflation rate. A surgery that cost ₹3 lakh in 2020 now approaches ₹6 lakh in a metropolitan hospital.

A well-structured family floater health insurance plan addresses hospitalisation costs, pre and post-hospitalisation expenses, maternity and newborn coverage, daycare procedures, and mental health treatments under newer plans.

🏥

♻️

🤱

💰

⏱️

This guide evaluated seven of India’s top insurers — Niva Bupa, HDFC ERGO, Care Health, Star Health, ICICI Lombard, Aditya Birla Health, and Tata AIG — across 14 parameters. No insurer has paid for placement here.

“The single biggest mistake Indian families make in 2026 is underinsuring — buying a ₹5 lakh floater for a family of four in a metro. We recommend a minimum of ₹20 lakh in Tier-1 cities, with a super top-up rider as a cost-effective supplement.”

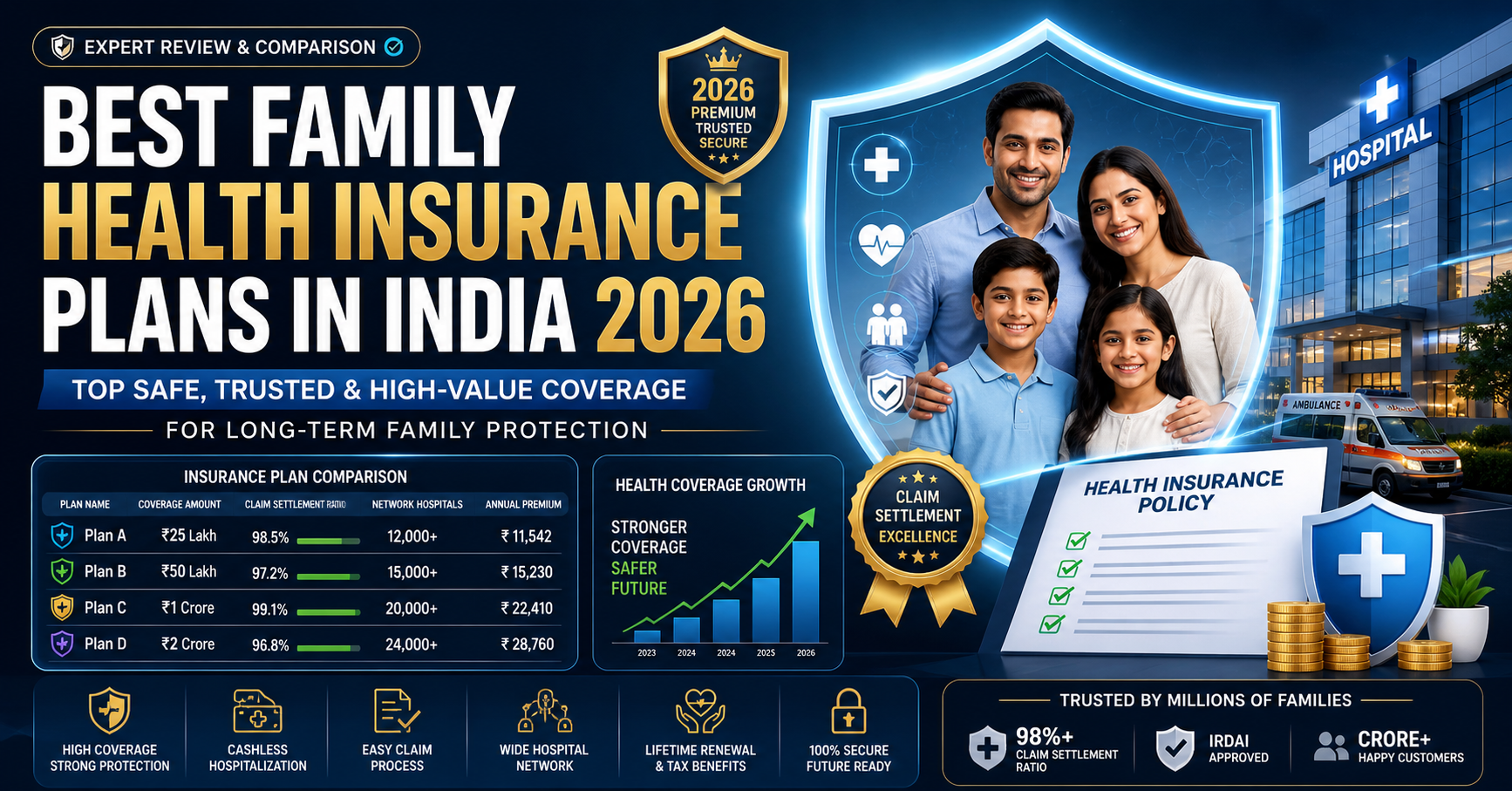

Best Family Health Insurance Plans India 2026: Quick Comparison Table

Use this snapshot to identify the best-fit insurer before diving into full plan reviews. All data is based on standard floater plans for a 35-year-old couple + 2 children, as of May 2026.

| Insurer / Plan | Best For | Sum Insured | Annual Premium* | Maternity | PED Wait | Restoration | Cashless Hospitals | CSR 2024–25 |

|---|---|---|---|---|---|---|---|---|

| Niva Bupa ReAssure 2.0 | Best Overall | ₹3L–₹1Cr | ₹18,000–₹32,000 | Yes | 36 months | Unlimited | 10,000+ | 91.2% |

| HDFC ERGO Optima Secure | Premium Coverage | ₹5L–₹2Cr | ₹22,000–₹45,000 | Yes | 36 months | 4× base SI | 13,000+ | 92.7% |

| Care Supreme Floater | Value + Maternity | ₹5L–₹6Cr | ₹15,000–₹28,000 | Yes | 24 months ✅ | Yes | 19,000+ ✅ | 90.4% |

| Star Family Health Optima | Budget Families | ₹3L–₹25L | ₹12,000–₹22,000 | Add-on | 48 months | Once/year | 14,000+ | 88.9% |

| ICICI Lombard Health Advantage | Digital-First | ₹5L–₹50L | ₹17,000–₹30,000 | Yes | 36 months | Yes | 10,900+ | 89.5% |

| Aditya Birla Activ Health Platinum | Wellness + Chronic | ₹5L–₹2Cr | ₹20,000–₹38,000 | Yes | 36M (chronic: 0) | Yes | 10,000+ | 90.0% |

| Tata AIG MediCare Premier | Global + High SI | ₹5L–₹3Cr | ₹19,000–₹42,000 | Yes | 36 months | Yes | 10,000+ | 91.8% |

*Indicative premiums for family of 4. Actual premiums vary by age, city, PEDs and add-ons. CSR = Claim Settlement Ratio. Source: IRDAI Annual Report 2024–25.

Which Plan Should YOU Choose? (Decision Engine)

Match your family profile to the right plan in seconds. This decision table is based on 14 evaluation parameters across all 7 insurers.

| Your Situation | Best Plan | Key Reason |

|---|---|---|

| 💰 Budget under ₹15,000/year | Star Family Health Optima | Lowest premium, large network |

| 🏙️ Family of 4 in metro city | HDFC ERGO Optima Secure | 92.7% CSR + 4× SI + 13,000 hospitals |

| 🤱 Pregnancy planning in 2–3 years | Care Supreme Floater | 24-month PED + maternity + 19,000 hospitals |

| ⚖️ Balanced value for nuclear family | Niva Bupa ReAssure 2.0 | Unlimited restoration + transparent terms |

| 🩺 Diabetic / BP / chronic conditions | Aditya Birla Activ Health | Day-1 chronic cover + wellness returns |

| ✈️ NRI / frequent international travel | Tata AIG MediCare Premier | Global emergency + ₹3Cr SI option |

| 📱 Tech-first, digital claims preferred | ICICI Lombard Health Advantage | 2-hour cashless approval, best app experience |

| 📊 Maximum Section 80D tax saving | HDFC ERGO Optima Secure | Higher SI = higher deduction at 30% slab |

| 👴 Parents aged 60+ to insure | Separate Senior Citizen Plan | Avoid depleting family floater SI |

No single plan wins for every family. Your profile — city tier, health history, maternity timeline, and budget — determines the right choice. Use the table above as your starting filter, then read the full review for your shortlisted plan.

Get Personalised Quotes in 2 Minutes

Compare live premiums from all 7 insurers — customised for your family’s age, city and health profile. Free, unbiased, no spam.

Top 7 Best Family Health Insurance Plans in India 2026 — Full Reviews

#1 — Niva Bupa ReAssure 2.0 Floater

🏆 Best Overall 2026

Niva Bupa ReAssure 2.0 leads our 2026 rankings with industry-defining unlimited restoration of sum insured — even for the same illness — combined with no room rent sub-limits from ₹15 lakh onwards.

Key Benefits

- Unlimited restoration including same illness

- No room rent cap from ₹15L SI onwards

- Booster benefit and digital cashless approval

- Maternity cover after 24 months, newborn from Day 1

✅ Pros

- Market-leading restoration

- Transparent policy wording

- Strong renewal benefits

❌ Cons

- Senior parents raise premium

- 36-month PED wait

- Maternity sub-limit may be low in metros

❌ Who Should Avoid

- Families needing PED coverage sooner than 36 months

- Buyers looking for the absolute lowest premium

#2 — HDFC ERGO Optima Secure

🥈 Best Premium Plan

HDFC ERGO Optima Secure is built for families wanting maximum coverage without compromise, with a signature 4× sum insured on Day 1, wide cashless network and the highest CSR in this comparison.

✅ Pros

- Highest CSR in this comparison

- 4× instant SI boost

- 13,000+ cashless hospitals

❌ Cons

- Higher premiums

- 36-month maternity wait

- Premium can rise with age

❌ Who Should Avoid

- Budget-constrained families with annual premium under ₹20,000

- Families planning pregnancy within 36 months (maternity wait applies)

#3 — Care Supreme Floater

🥉 Best Value + Maternity

Care Supreme offers a short 24-month PED waiting period and the widest cashless hospital network in this comparison, making it attractive for maternity planning and mild pre-existing conditions.

❌ Who Should Avoid

- Families prioritising unlimited restoration (not available in all variants)

- Those needing global emergency coverage

#4 — Star Family Health Optima

💰 Best Budget Plan

Star Family Health Optima is suited to budget-conscious young families in Tier-2 and Tier-3 cities, with affordability and a large hospital network but a longer PED wait.

❌ Who Should Avoid

- Families with existing conditions needing early coverage (48-month PED wait)

- Metro families needing sum insured above ₹25 lakh

- Families actively planning pregnancy (maternity is add-on only)

#5 — ICICI Lombard Health Advantage

📱 Best Digital Experience

ICICI Lombard Health Advantage is a strong mid-tier option for tech-forward families prioritising app-based claims, digital service and quick cashless processing.

❌ Who Should Avoid

- Families needing sum insured above ₹50 lakh

- Those preferring non-digital, branch-based claim support

#6 — Aditya Birla Activ Health Platinum Enhanced

🏃 Best Wellness + Chronic

Aditya Birla Activ Health Platinum Enhanced rewards wellness activity and is notable for chronic condition coverage features in selected variants.

❌ Who Should Avoid

- Families with sedentary lifestyles (wellness rewards require activity tracking)

- Those needing unlimited restoration (not a core feature)

#7 — Tata AIG MediCare Premier

🌍 Best Global + High SI

Tata AIG MediCare Premier is suited to high-income families wanting global emergency coverage, high sum insured options and limited sub-limits.

❌ Who Should Avoid

- Budget-focused Tier-2/3 families (premium is higher)

- Those not needing global coverage (you pay for features you may not use)

Which Health Insurance Actually Pays Claims Smoothly in 2026?

Claim settlement ratio alone does not reflect real claim experience. In 2026, Indian families must evaluate payout consistency, approval speed, sub-limit deductions, and real-world denial rates — not just headline CSR numbers.

⚡ 2h

⚡ 2h

⚡ 2h

⏳ 3.2h

⏳ 3.5h

⏳ 4h

| Insurer | CSR 2024–25 | Avg Cashless TAT | Hidden Deduction Risk | Room Rent Cap |

|---|---|---|---|---|

| HDFC ERGO | 92.7% 🏆 | 2.1 hours | Low | None (higher SI) |

| Tata AIG | 91.8% | 3.2 hours | Low | None (Premier) |

| Niva Bupa | 91.2% | 2.0 hours | Low | None (₹15L+) |

| Care Health | 90.4% | 4.0 hours | Medium | Varies by variant |

| Aditya Birla | 90.0% | 3.5 hours | Medium | Check variant |

| ICICI Lombard | 89.5% | 2.0 hours | Medium | Check variant |

| Star Health | 88.9% | 5.5 hours | Higher risk | Sub-limits apply |

“The three questions that actually matter: (1) What is the room rent limit? (2) Are there disease-specific sub-limits? (3) Is there a co-payment clause? A plan with 92% CSR and heavy sub-limits can pay less than a plan with 89% CSR and no sub-limits.”

How to Choose the Best Family Health Insurance Plan in 2026

1. Get the Sum Insured Right First

Underinsuring is the costliest mistake Indian families make. Here is our 2026 city-tier guidance:

₹20–25LTier-1 Cities

₹10–15LTier-2 Cities

₹5–10LTier-3 Cities

Pair your base plan with a super top-up plan for cost-efficient high coverage. A ₹15L base + ₹85L super top-up can be cheaper than a standalone ₹1 crore plan.

2. Critical Features Checklist

| Feature | What to Look For | Red Flag to Avoid |

|---|---|---|

| Room Rent Cap | No sub-limit, or ≥1% of SI/day | ₹3,000/day cap |

| Co-Payment | Zero co-pay | 20%+ co-pay |

| Restoration | Unlimited, same illness covered | One-time only |

| Hospital Network | 10,000+ nationally | Under 5,000 hospitals |

| PED Wait | Under 36 months | 48+ months |

| Maternity Wait | Under 24 months | 36+ months |

| CSR | Above 90% | Below 85% |

3. Senior Parent Inclusion Warning

A family floater works best for young families. Always buy a separate senior plan for parents over 60.

“The optimal 2026 strategy for a metro family of four: ₹15L floater + ₹85L super top-up + separate senior plan for parents 60+.”

How We Selected These Plans (Our Methodology)

This guide is based on an independent evaluation of 7 major insurers across 14 parameters. No insurer has paid for inclusion, ranking, or favourable treatment.

Best Family Health Insurance Plans by Use Case

Family of 3

Young couple + 1 child, metro city

✅ Niva Bupa ReAssure 2.0

Family of 4

Parents + 2 children, metro city

✅ HDFC ERGO Optima Secure

Senior Parents

Parents aged 60+ — always separate

✅ Separate Senior Plan

Under ₹15,000 Premium

Budget-conscious Tier-2 families

✅ Star Family Health Optima

Best Maternity Plan

Planning pregnancy in 2–3 years

✅ Care Supreme Floater

High Coverage ₹25L+

Metro HNI and high-risk families

✅ Tata AIG MediCare Premier

Best Tax-Saving Plan

Maximum Section 80D benefit

✅ HDFC ERGO Optima Secure

Best Wellness Plan

Diabetics, BP patients, fit families

✅ Aditya Birla Activ Health

💬 Talk to an Expert Advisor

Our insurance desk helps families choose the right plan. Free, unbiased, zero obligation.

Family Floater vs Individual Health Insurance Policies

Family Floater

One premium covers the entire family under a shared sum insured. Cost-efficient for young, healthy families.

- ✅ One premium, full family covered

- ✅ Cost-effective under age 45

- ✅ Simpler renewals

- ❌ Shared SI can deplete

- ❌ One high-risk member raises premium

Individual Policies

Each member gets dedicated sum insured. Better when ages vary significantly or someone has serious PEDs.

- ✅ Dedicated SI per member

- ✅ One claim doesn’t affect others

- ✅ Essential for senior parents

- ❌ Higher combined premium

- ❌ More policies to manage

Tax Benefits Under Section 80D: Complete 2026 Guide

Health insurance premiums qualify for tax deductions under Section 80D of the Income Tax Act, 1961. Available under the old tax regime only.

₹25,000Self + Spouse + Children

₹25,000Parents below 60

₹50,000Senior Parents 60+

₹75,000Maximum Total Deduction

Tax Planning Example (FY 2025–26)

| Profile | Premium Paid | 80D Deduction | Tax Saved (30% slab) |

|---|---|---|---|

| Self + Spouse + 2 Kids | ₹22,000 | ₹22,000 | ₹6,600 |

| Self + Family + Non-Senior Parents | ₹22,000 + ₹20,000 | ₹42,000 | ₹12,600 |

| Self + Family + Senior Parents | ₹22,000 + ₹42,000 | ₹75,000 max | ₹22,500 |

Tax savings calculated at 30% slab. Source: Income Tax India — Section 80D.

📈 Related Financial Guides

Tax Savings + Wealth Building: Banking & Finance Cluster

Health insurance gives you tax deductions. Combine that strategy with smart banking investments for total financial protection in 2026.

Claim Settlement & Cashless Network Analysis 2026

A plan is only as good as the claim it pays. Below is the CSR and network data from IRDAI Annual Report 2024–25.

| Insurer | CSR 2024–25 | Avg Cashless TAT | Cashless Hospitals | Digital Claims |

|---|---|---|---|---|

| HDFC ERGO | 92.7% 🏆 | 2.1 hours | 13,000+ | Yes |

| Tata AIG | 91.8% | 3.2 hours | 10,000+ | Yes |

| Niva Bupa | 91.2% | 2.0 hours | 10,000+ | Yes |

| Care Health | 90.4% | 4.0 hours | 19,000+ | Yes |

| Aditya Birla | 90.0% | 3.5 hours | 10,000+ | Yes |

| ICICI Lombard | 89.5% | 2.0 hours | 10,900+ | Yes |

| Star Health | 88.9% | 5.5 hours | 14,000+ | Partial |

Always verify your preferred hospitals are on the insurer’s cashless empanelled list before purchase.

Common Exclusions & Costly Buyer Mistakes

1. Room Rent Cap — The Silent Claim Killer

Many budget plans cap room rent at ₹3,000–5,000/day. If you stay in a room above the cap, the insurer may apply proportionate deduction to the entire bill.

2. Non-Disclosure of Pre-Existing Conditions

Failing to disclose diabetes, hypertension, thyroid disorders, or past surgeries can result in claim rejection. Always disclose everything.

3. Standard Exclusions Across All Plans

- Cosmetic procedures: usually not covered

- Self-inflicted injuries: excluded

- War and nuclear perils: standard exclusion

- Weight loss treatment: excluded unless medically necessary

- Adventure sports injuries: excluded unless rider added

- First 30 days: non-accident claims excluded

- Specific disease waiting: hernia, cataracts and joint replacements often have waits

4. Low Sum Insured for Metro Cities

A ₹5 lakh floater for Mumbai or Delhi in 2026 is dangerously inadequate. Serious hospitalisation costs can exceed ₹10–15 lakh.

FAQ — Best Family Health Insurance Plans India 2026: 18 Top Questions

Which are the best family health insurance plans India 2026?

The best family health insurance plans India 2026 include Niva Bupa ReAssure 2.0, HDFC ERGO Optima Secure, and Care Supreme Floater depending on your family profile, maternity needs, cashless hospital network, and budget.

What is a family floater health insurance plan?

A family floater health insurance plan covers all specified family members under one shared sum insured. Any member can use the full sum insured, or it can be split across multiple claims in the same policy year.

Is ₹10 lakh enough for family health insurance in India in 2026?

For Tier-2 and Tier-3 cities, ₹10 lakh may be adequate for a young, healthy family. For Tier-1 cities like Delhi, Mumbai, Bengaluru, Chennai, and Hyderabad, ₹20–25 lakh is safer. Supplement with a super top-up for catastrophic protection.

Can I include my parents in a family floater plan?

You can, but it is usually not advisable for parents aged 60+. Adding senior parents can increase the entire family premium and may deplete the shared sum insured quickly. A separate senior citizen plan is usually better.

Which plan has the best maternity cover in India 2026?

Care Supreme Floater offers a strong maternity combination with a 24-month waiting period. Niva Bupa ReAssure 2.0 also offers maternity cover after 24 months with newborn coverage after birth.

Which insurer has the best claim settlement ratio in India 2026?

Based on the data used in this guide, HDFC ERGO leads among the compared private insurers with a 92.7% claim settlement ratio, followed by Tata AIG (91.8%) and Niva Bupa (91.2%).

Are family health insurance premiums tax deductible in India?

Yes. Under Section 80D, premiums are deductible under the old tax regime. You can claim up to ₹25,000 for self and family, plus an additional deduction for parents depending on their age — up to ₹75,000 total if parents are senior citizens.

What is PED waiting period and why does it matter?

PED means pre-existing disease. The waiting period is the time you must wait before claims related to existing conditions like diabetes, hypertension, asthma, or thyroid disorders are covered. Most plans have 24–48 month PED waits. Care Supreme Floater offers the shortest at 24 months.

What is restoration benefit in family health insurance?

Restoration benefit refills your sum insured after it is exhausted by a claim. This is useful in family floater policies where more than one family member may need hospitalisation in the same year. Niva Bupa ReAssure 2.0 offers unlimited restoration even for the same illness.

Should I buy separate health insurance for parents?

Yes, especially if your parents are aged 60 or above. A dedicated senior citizen policy gives them separate coverage and protects your family floater from being exhausted by one large claim. It also typically leads to lower premiums for your main family floater.

What is a co-payment clause and should I avoid it?

A co-payment clause means you pay a fixed percentage of every claim yourself. For working-age adults, zero co-pay plans are usually better. Co-pay may be acceptable in some senior citizen plans where it helps reduce overall premiums.

What is No-Claim Bonus (NCB) in health insurance?

No-Claim Bonus increases your sum insured for every claim-free year, usually without extra premium. Always check whether the bonus reduces after a claim year and whether it accumulates cumulatively or resets.

Can I buy family health insurance online in India?

Yes. You can buy policies online through insurer websites or IRDAI-licensed brokers and aggregators. Avoid unverified third-party platforms. Always verify the insurer’s IRDAI registration before purchasing.

What sum insured is ideal for a family in Bengaluru in 2026?

For a family of four in Bengaluru, ₹20 lakh is a sensible minimum. Families with senior members or chronic conditions may need ₹25–30 lakh or a base policy plus super top-up combination.

What are daycare treatments in health insurance?

Daycare treatments are medical procedures that require hospitalisation for less than 24 hours, such as cataract surgery, dialysis, chemotherapy, and certain arthroscopy procedures. Most modern plans cover 540+ daycare procedures.

Which plan gives the fastest claim approval in 2026?

ICICI Lombard and Niva Bupa are among the fastest for cashless claim approval, averaging around 2 hours at network hospitals. HDFC ERGO also performs at approximately 2.1 hours. Star Health has a slower average of around 5.5 hours.

Which insurer has the least complaints in India 2026?

HDFC ERGO and Niva Bupa consistently rank lowest in consumer grievances among private health insurers, based on IRDAI complaints data for 2024–25. Always check the IRDAI grievance redressal data before purchasing.

Is ₹20 lakh enough for a family in 2026?

₹20 lakh is a reasonable base for Tier-1 metro cities for a healthy family of four. If you have senior members, chronic conditions, or want truly comprehensive protection, consider ₹25–30 lakh base or combine a ₹15L floater with a super top-up. With 13% medical inflation in 2026, ₹20L provides a solid but not unlimited safety net.

Glossary: Key Health Insurance Terms Explained

- Family Floater Plan

- A single policy covering specified family members under one shared sum insured.

- Pre-Existing Disease (PED)

- A medical condition diagnosed, treated or symptomatic before the policy start date.

- Restoration Benefit

- Automatic refilling of sum insured after it is exhausted by a claim.

- Cashless Claim

- The insurer pays the network hospital directly, reducing upfront payment.

- Co-Payment

- A percentage of every claim the policyholder must pay out of pocket.

- Room Rent Cap

- A daily room rent limit. Exceeding it can trigger proportionate deductions.

- Section 80D

- Income Tax Act provision allowing premium deduction under the old tax regime.

- Maternity Waiting Period

- Minimum policy duration before maternity expenses are covered.

- Claim Settlement Ratio

- Percentage of claims approved by an insurer in a financial year.

- Super Top-Up Plan

- An add-on policy that activates after your deductible or base cover is exhausted.

- No-Claim Bonus

- Annual increase in sum insured for claim-free years.

- IRDAI

- Insurance Regulatory and Development Authority of India. Official website →

Final Expert Verdict: Best Family Health Insurance Plans India 2026

After evaluating seven insurers across 14 parameters, here are our recommendations by profile:

“Buy now — not later. Every year of delay means higher premiums at a higher age, and the risk that a new diagnosis becomes a pre-existing condition.”

🚀 Protect Your Family Today

Get free personalised quotes from all 7 top insurers in under 2 minutes. Expert advisory available.

Join PositionalCalls WhatsApp Channel

Get unbiased insurance analysis, plan alerts, premium changes, and expert breakdowns — straight to WhatsApp.

📚 Sources & References

- IRDAI Annual Report 2024–25 — Claim Settlement Ratios and Market Data

- Income Tax India — Section 80D Official Resource

- Official policy brochures: Niva Bupa, HDFC ERGO, Care Health, Star Health, ICICI Lombard, Aditya Birla Health, Tata AIG (May 2026)

- India Medical Inflation Report 2025 — National Insurance Academy, Pune

- IRDAI Health Insurance Regulatory Framework — Consumer Guidelines 2025

Shubham tracks Indian equity markets with a focus on banking stocks, insurance companies, and long-term value investing. PositionalCalls was built to give independent investors the same quality of research that institutional desks produce — in plain language, with no brokerage bias and no paid promotions. All analysis is sourced from RBI, SEBI, NSE/BSE filings, and company annual reports.