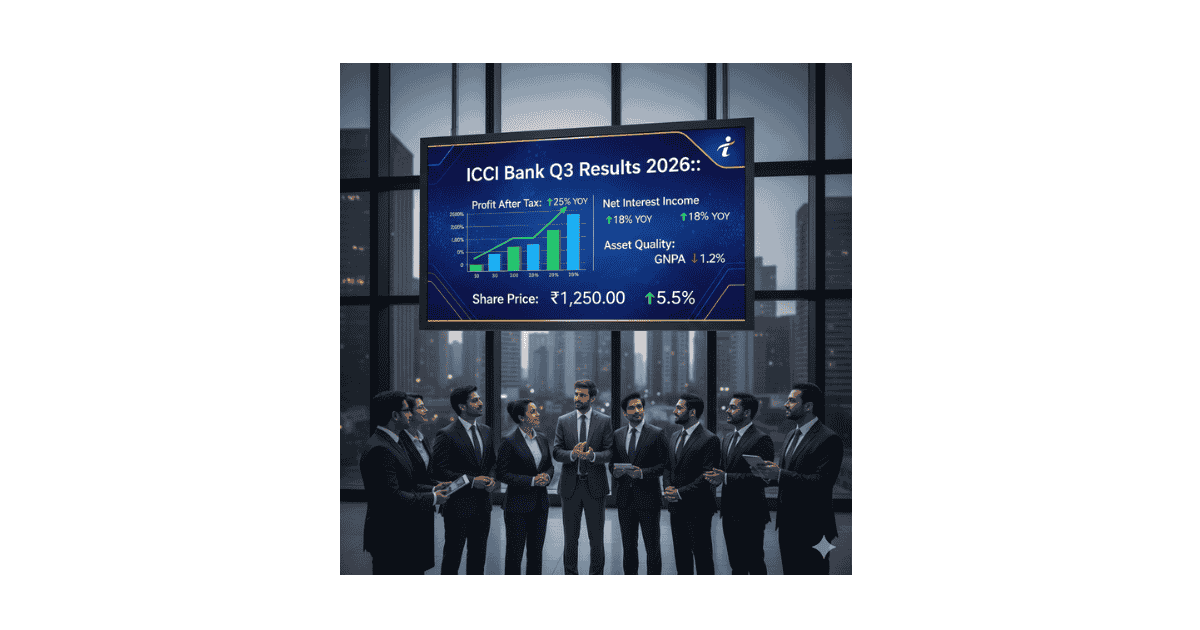

ICICI Bank Q3 Results 2026: Profit Growth, NIM, Asset Quality & Full Analysis

ICICI Bank Q3 Results 2026: Profit at ₹11,318 Crore, Asset Quality Improves Last updated: February 2026 ICICI Bank Q3 Results 2026 highlight strong profit growth, stable asset quality, and continued retail loan momentum, reinforcing the bank’s leadership in private banking. India’s second-largest private bank reported steady earnings, improved asset quality, and strong capital ratios in … Read more