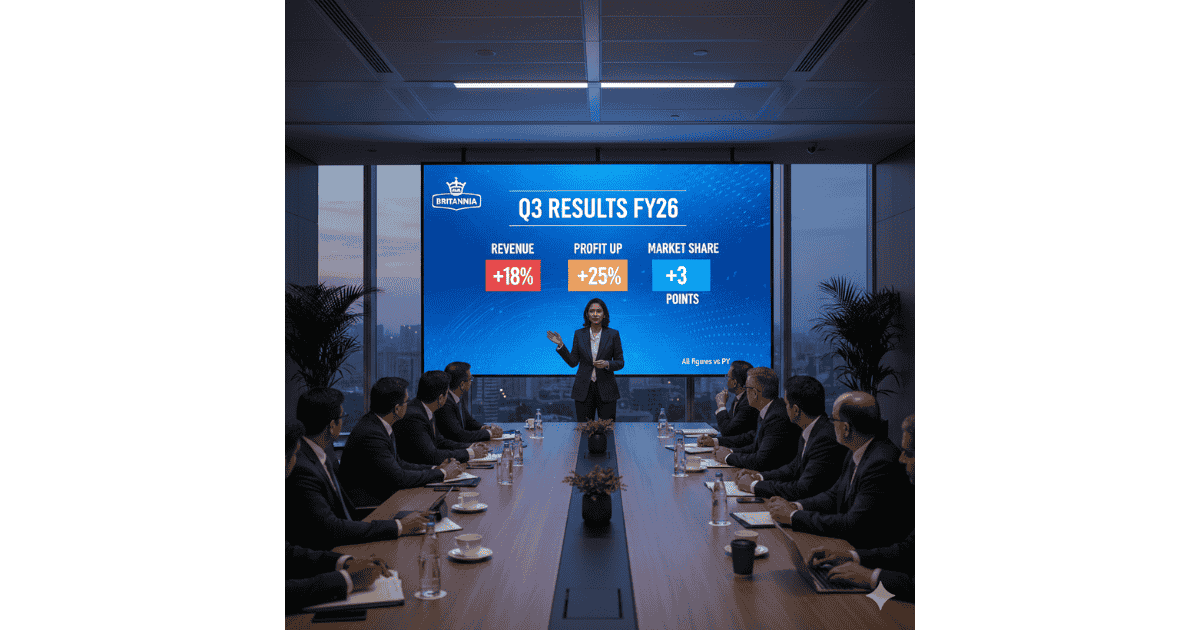

Britannia Q3 Results FY26: Profit Rises to ₹682 Crore on Strong Foods Portfolio

Last updated: February 2026

Britannia Q3 Results FY26 reflect steady profit performance, improving margins, and stable demand across key product categories.

Results Snapshot (Official Filing)

- Company: Britannia Industries Limited

- Quarter: Q3 FY26 (December 2025)

- Revenue from operations: ₹4,969.82 crore

- Profit before tax: ₹919.03 crore

- Net profit: ₹682.14 crore

- Q3 FY25 net profit: ₹582.30 crore

- Earnings per share: ₹28.23

Britannia Q3 Results FY26: Key Highlights

Britannia Industries reported consolidated net profit of ₹682.14 crore for the quarter ended December 2025, compared to ₹582.30 crore in the same period last year. Revenue from operations stood at ₹4,969.82 crore, reflecting steady growth across its core foods portfolio. These figures are based on the company’s official unaudited consolidated financial results.

The company continues to benefit from strong demand across its biscuit, dairy, and packaged foods categories, supported by brand strength and distribution reach across urban and rural markets.

Britannia Q3 Results FY26: Quarterly Financial Performance

| Metric | Q3 FY26 | Q3 FY25 | YoY Change |

|---|---|---|---|

| Revenue from operations | ₹4,969.82 crore | ₹4,592.62 crore | +8.2% |

| Profit before tax | ₹919.03 crore | ₹778.39 crore | +18.1% |

| Net profit | ₹682.14 crore | ₹582.30 crore | +17.1% |

The company delivered strong profit growth during the quarter, with operating leverage supporting margins despite cost pressures.

Britannia Q3 Results FY26: Cost Structure and Operating Performance

Total expenses during the quarter stood at ₹4,107.59 crore, compared to ₹3,874.65 crore in Q3 FY25. The increase was primarily driven by higher raw material costs, employee expenses, and other operational costs.

Key expense components

- Cost of materials consumed: ₹2,662.98 crore

- Employee benefits expense: ₹214.73 crore

- Finance costs: ₹33.25 crore

- Depreciation and amortisation: ₹84.51 crore

- Other expenses: ₹955.28 crore

Despite the increase in expenses, Britannia managed to expand profitability through improved product mix and operational efficiencies.

Britannia Q3 Results FY26: Profitability Trends

Britannia’s profit before tax rose to ₹919.03 crore in Q3 FY26, compared to ₹778.39 crore in the same quarter last year. Net profit increased to ₹682.14 crore, reflecting improved operating margins and cost management.

The company’s net profit margin for the quarter stood at approximately 13.7%, compared to 12.7% in Q3 FY25, indicating margin expansion during the quarter.

Britannia Q3 Results FY26: Balance Sheet and Capital Structure

Britannia continues to maintain a strong balance sheet, with low leverage and consistent cash-flow generation. The company’s stable capital structure supports regular dividends and long-term expansion plans.

The company reported earnings per share of ₹28.23 for the quarter, compared to ₹24.15 in the same quarter last year.

Sector Context: Consumption and FMCG Outlook

The FMCG and consumption sector remains one of the most defensive and high-quality segments in the Indian equity market. Stable demand, strong brand equity, and consistent cash flows make large FMCG companies attractive to institutional investors.

For a broader sector view, read the Consumption Sector Outlook 2026.

Consumption Sector Outlook 2026

Consumption Sector Hub

Source: Britannia Q3 FY26 results as filed with the NSE.

Britannia Q3 FY26

Peer Comparison

Britannia’s performance can be compared with other large consumption companies:

Britannia Q3 Results FY26: Business Model Overview

Britannia operates primarily in the packaged foods segment, with a strong portfolio across biscuits, cakes, dairy, and other food categories. The company has a wide distribution network across India and international markets.

Its strong brand portfolio, pricing power, and distribution strength enable it to maintain stable margins and consistent growth across economic cycles.

Institutional View: What the Results Signal

Britannia’s Q3 FY26 results reinforce the strength of the consumption sector. The company continues to benefit from:

- Stable demand for packaged foods

- Strong brand equity

- Wide distribution network

- Consistent cash-flow generation

Key Positives

- Strong revenue growth

- Profit growth above revenue growth

- Margin expansion

- Low leverage balance sheet

- Strong brand portfolio

Key Risks

- Raw material cost volatility

- Competitive intensity in biscuits and packaged foods

- Rural demand fluctuations

Valuation and Institutional Outlook

FMCG companies typically trade at premium valuations due to their stable earnings profiles. Britannia’s strong margins, brand strength, and cash-flow generation support its long-term investment appeal.

Future growth drivers include:

- Premium product launches

- Rural distribution expansion

- Product innovation

- International market growth

Final Verdict: Institutional Take

| Factor | Assessment |

|---|---|

| Revenue growth | Stable |

| Profitability | Strong |

| Balance sheet | Healthy |

| Sector outlook | Positive |

| Institutional stance | Defensive compounder |

Britannia’s Q3 FY26 results reinforce its position as a stable, high-quality FMCG player with strong profitability and consistent demand across its core foods portfolio.